Monthly Investment Insights - May 2025

Liberation Day

Source: Bloomberg

Market Review

April 2025 saw volatility reminiscent of the 2020 Covid crisis, as President Trump’s “Liberation Day” tariffs imposed a 10% baseline levy on all imports and much higher rates on key trading partners, escalating global trade tensions and triggering sharp swings across markets. Despite a steep intra-month selloff, the S&P 500 ended down just 0.76% and the Nasdaq gained 1.52%, buoyed by intermittent tariff exemptions and negotiation hopes. However, these aggressive and unpredictable trade measures sparked an unprecedented loss of confidence in US assets: the dollar index plunged over 4% to a three-year low, and US Treasury volatility spiked as global investors questioned the credibility and safe-haven status of both the dollar and Treasuries in the face of mounting policy and fiscal risks.

China remained resilient in the face of new US tariffs, swiftly responding with reciprocal duties on US goods-raising rates up to 125%, while mobilising a RMB 500 billion stabilisation fund, broad rate cuts, and fiscal stimulus to support markets and economic stability. Concurrently, President Xi travelled to Southeast Asia to deepened ties through new trade agreements. Domestically, patriotic sentiment surged as citizens promoted direct factory sales and invested in local equities. As a result, the CSI 300 finished the month virtually flat at -0.07%, underscoring China’s preparedness and resilience despite being a primary target of this latest round of US tariffs.

Performance

My April exposure performed relatively well, with surprising nuances in certain asset classes. US equities were nearly flat at -0.3% after an intra-month swing low of -13%, reflecting the whipsaw effects of Liberation Day. The nuclear sector rebounded strongly, up 7.7%, as global demand normalised and the IEA projected record nuclear generation for 2025. In contrast, US Treasuries-traditionally a safe haven-fell 1.4% amid a crisis of confidence in US assets and concerns over fiscal credibility. Ethereum declined 2.2% as investors rotated out of secondary thematics during heightened uncertainty, while Bitcoin surged 14.3%, shifting from a tech-correlated risk asset to a perceived hedge against instability in the US financial system, as it was originally created for. Mortgage-backed securities offered modest stability, returning 0.4%.

Outlook

May is shaping up to be an optimistic month. The last day of April offered an early signal: despite a Q1 GDP contraction, which was largely due to a temporary pre-tariff import surge; underlying momentum remains solid with the Atlanta Fed now projecting 2.4% Q2 growth. Meanwhile, software giants like Netflix, Microsoft, and Meta reported robust earnings, highlighting the sector’s resilience and minimal exposure to global tariffs. This strength in software aligns with my thematic focus for 2025, as technology and digital platforms continue to drive growth despite trade tensions.

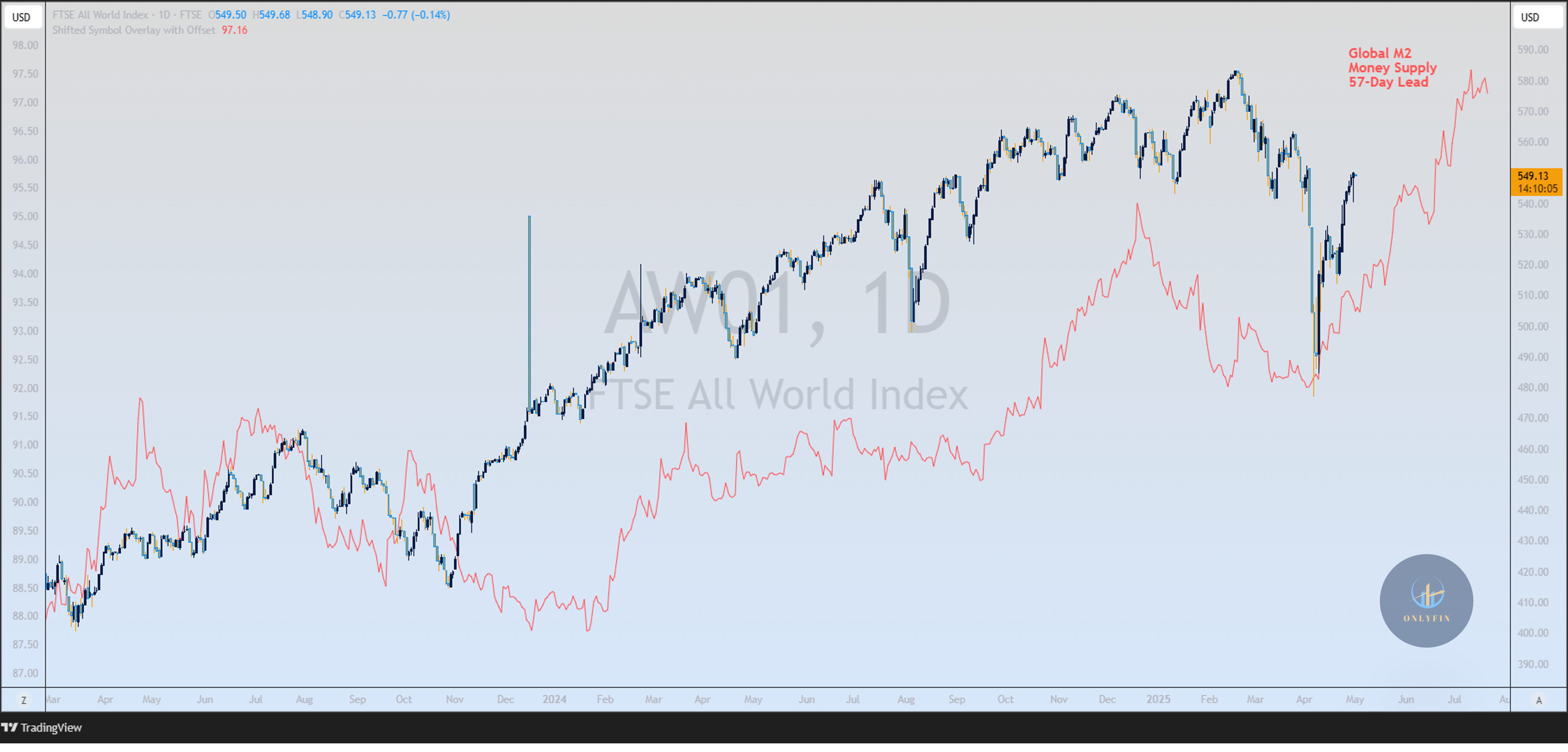

The chart above highlights that global M2 money supply has been rising steadily since January 2025, even as the Federal Reserve has held off on cutting interest rates. This expansion in liquidity is being driven by other major central banks like the ECB, BOJ, and PBOC easing policy and injecting funds into the system. Historically, increases in global M2 tend to flow into risk assets like equities and Bitcoin after a lag of about 57 days, signaling potential upside for markets in the months ahead. This implies the Fed put is still in play as well as the Trump put, as he backs away from an all-out trade war. As such, the environment remains supportive for risk assets as global liquidity continues to underpin market resilience.

Allocation

For May, I maintain a constructive outlook on US equities, supported by improving economic data and a continued rise in global liquidity. However, I am cautious on long-term US Treasuries due to the recent crisis of confidence, and are rotating into global bonds which offer more attractive risk-adjusted returns in the current environment. In line with this more defensive stance on US yield assets, I am shifting from US mortgage-backed securities to Singapore REITs, which provide comparable yields with less US concentration and benefit from topping interest rates. I continue to favour my 2025 thematic exposures-nuclear energy, which is set for record global generation and robust investments, and digital assets, where regulatory progress and institutional adoption remain strong tailwinds as markets stabilise.

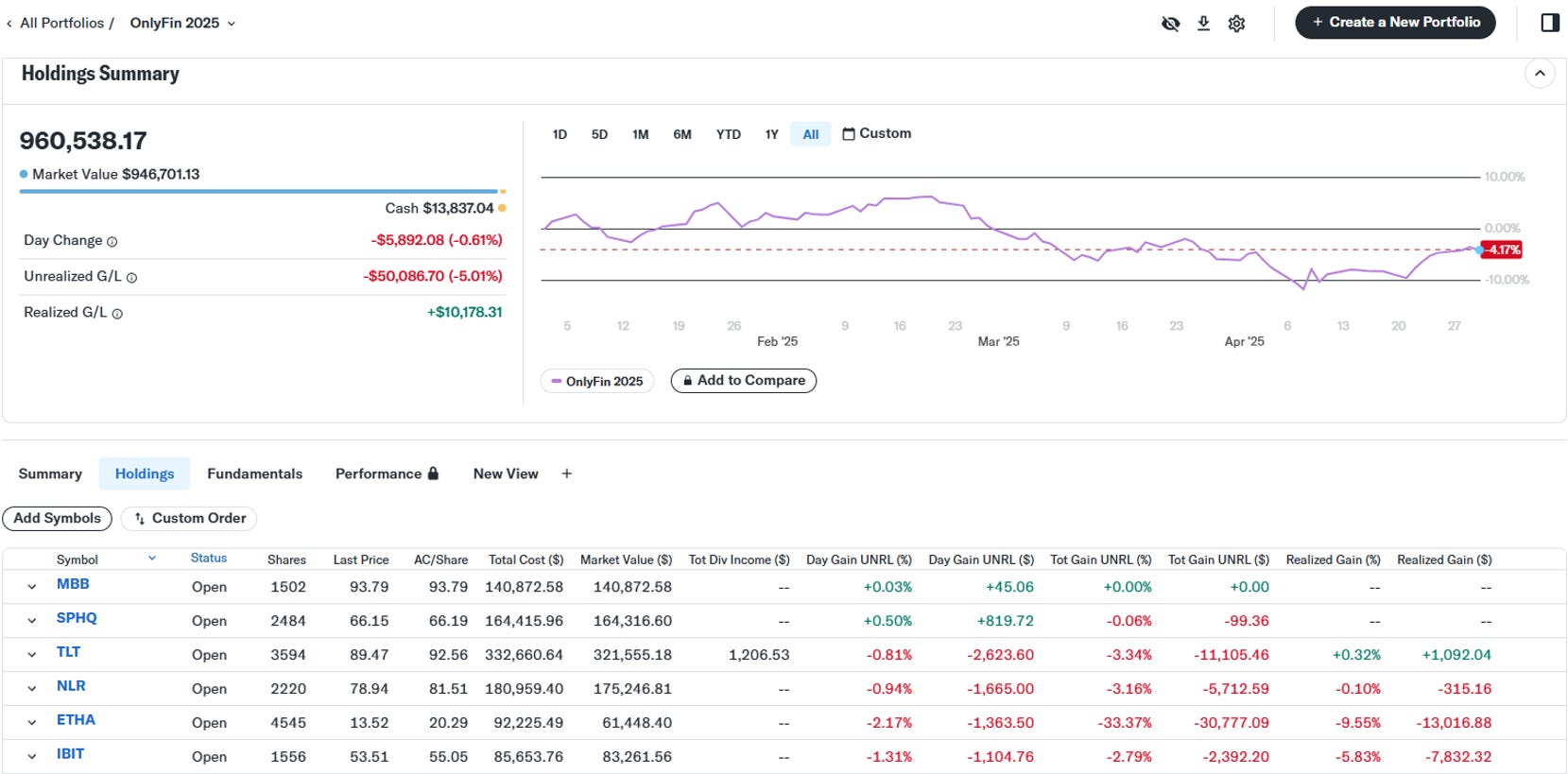

Overweight Picks & Performance

*Since 2 Jan 2025

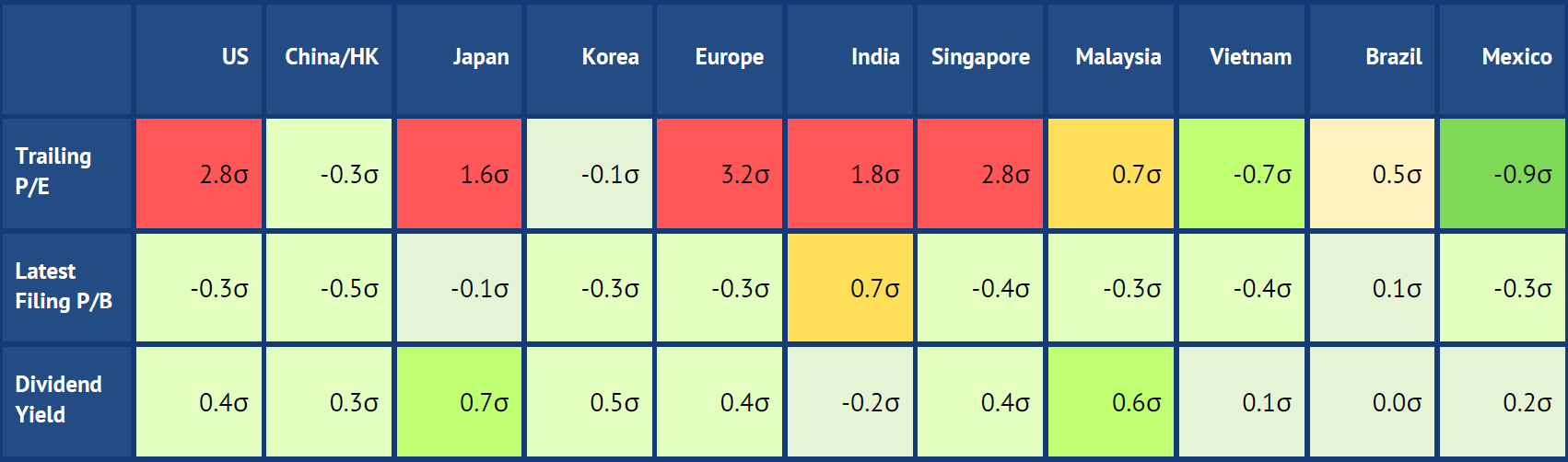

Valuations Snapshot

Current valuations

Relative to 10-year historical

Relative to Global Equities

Sources: Bloomberg, WorldPERatio

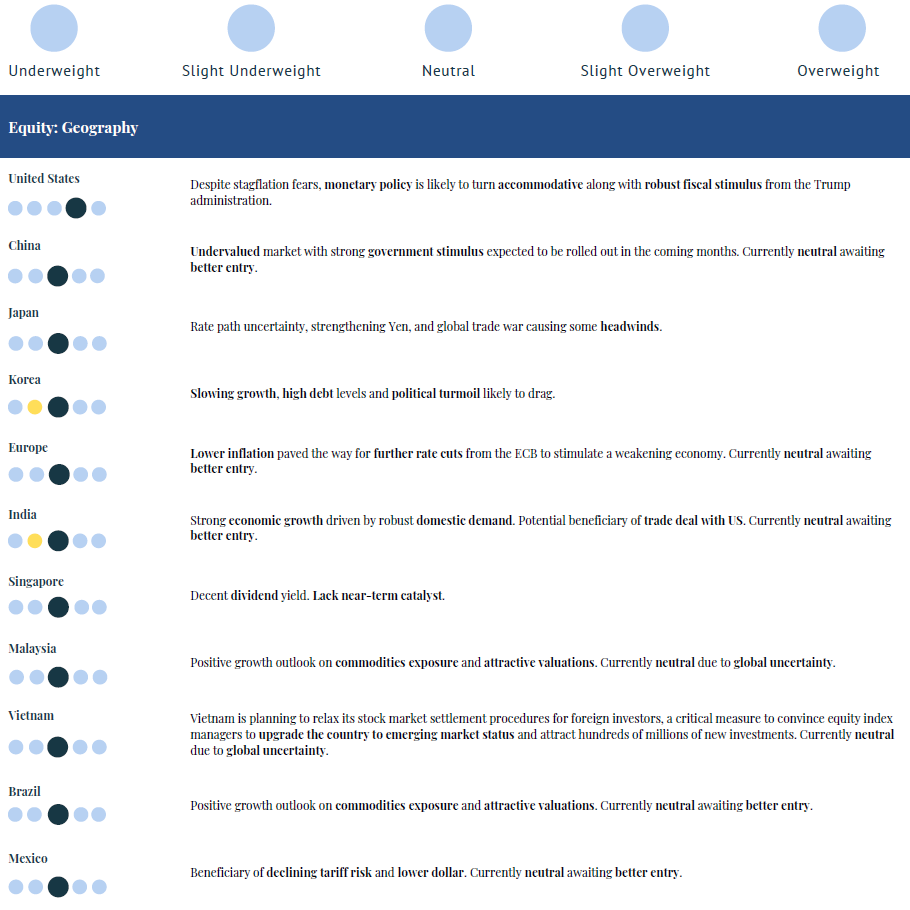

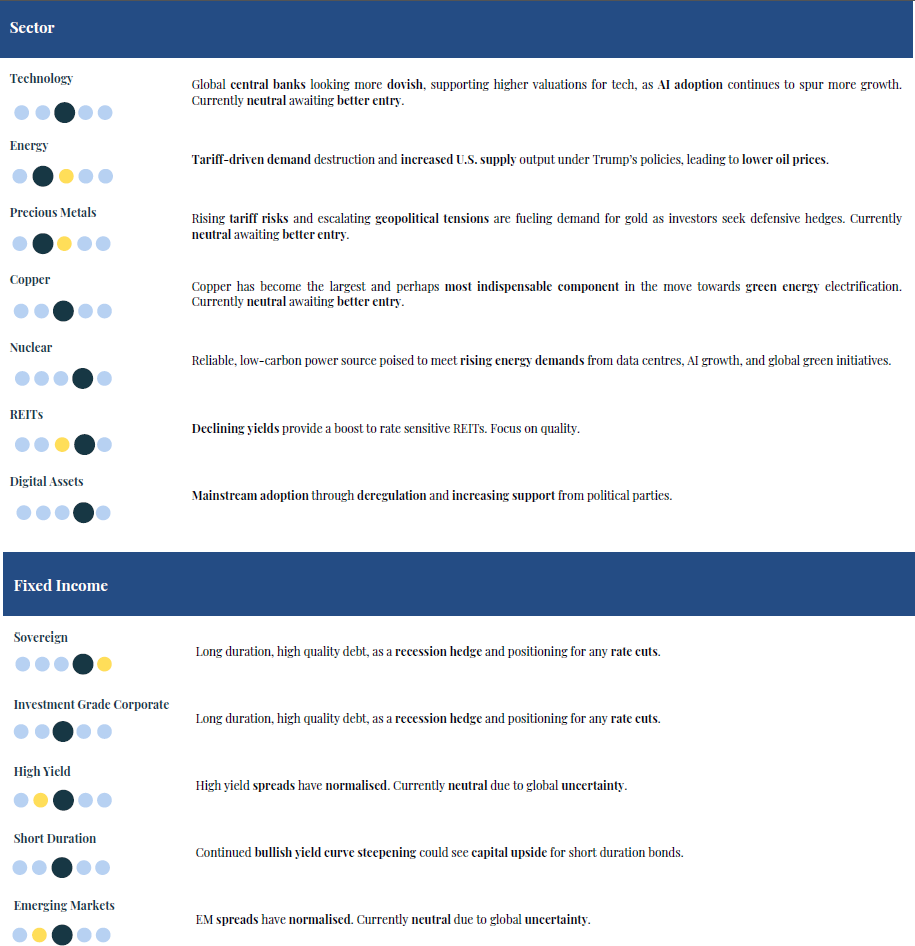

Tactical Views

Disclaimer

This publication is for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or risk tolerances of any of the recipients. The information or opinions provided are personal views and do not constitute investment advice, a recommendation, an offer, or solicitation to subscribe for, purchase, or sell the investment product(s) mentioned herein.