Monthly Investment Insights - Mar 2025

Is US Exceptionalism Over?

Source: Bloomberg

In February 2025, global equities diverged notably, with non-U.S. markets outperforming the U.S. The FTSE All-World ex US Index rose 4.98% year-to-date, while the S&P 500 gained 0.87%. This disparity intensified post-President Trump's January 20 inauguration, following the introduction of protectionist trade policies, including tariffs on imports from China, Canada, and Mexico. These measures have introduced uncertainty into the U.S. market, potentially contributing to its relative underperformance. Conversely, international markets have demonstrated resilience, suggesting that investors are seeking opportunities beyond U.S. borders in response to the evolving trade landscape.

In China, President Xi Jinping convened a symposium with business leaders, emphasizing the private sector's role in innovation amid U.S.-China tech tensions. Hong Kong announced a HK$1 billion AI Research and Development Institute to position the city as an AI hub. Alibaba reported a 7.6% revenue increase to RMB 280.15 billion, surpassing expectations and reaching a three-year share price high. These developments, alongside upcoming National People's Congress sessions, are poised to further bolster sectors that have lagged in the recent rally.

European markets showed resilience, partly due to expectations of increased defense spending and strategic initiatives aimed at reducing regulatory burdens and promoting key industries. In contrast, U.S. equities faced headwinds from weak retail sales, declining consumer confidence, and geopolitical tensions, leading to concerns over potential stagflation and dampening investor sentiment.

In February, my China/HK exposure surged 13.7% on strong earnings and policy support, while Mexico and Energy rose 6.5% and 3.9% respectively. Nuclear fell 11.3% as AI-driven energy demand was reassessed. My Bitcoin and Ethereum positions declined 11.3% and 13.5% respectively, pressured by a $1.4B ByBit hack and risk-off sentiments.

Looking ahead, March is anticipated to be range-bound as investors assess the implications of President Trump's recent policy decisions, including the imposition of 25% tariffs on imports from Mexico and Canada, effective March 4, and the doubling of tariffs on Chinese goods to 20%. Concurrently, the administration's Department Of Government Efficiency (DOGE) initiative has mandated federal agencies to develop plans for workforce reductions, leading to significant job cuts. These measures have introduced uncertainty into the markets, prompting a cautious investor stance.

The next upside catalyst likely hinges on the Trump administration’s stimulus measures. With tariffs and DOGE austerity in place, the focus shifts to balancing growth and inflation. Treasury Secretary Scott Bessent has signaled plans to lower US 10Y yields through deregulation, tax cuts, and lower oil prices, while Elon Musk considers government payouts from DOGE savings.

For March, I am positive on U.S. equities and long-term Treasuries, expecting stimulus measures to offset recent policy tightening. I see nuclear energy’s pullback as overdone, with structural demand intact, while digital assets stand to benefit from deregulation tailwinds and speculation around a potential U.S. Bitcoin Strategic Reserve.

Overweight Picks & Performance

*Since 2 Jan 2025

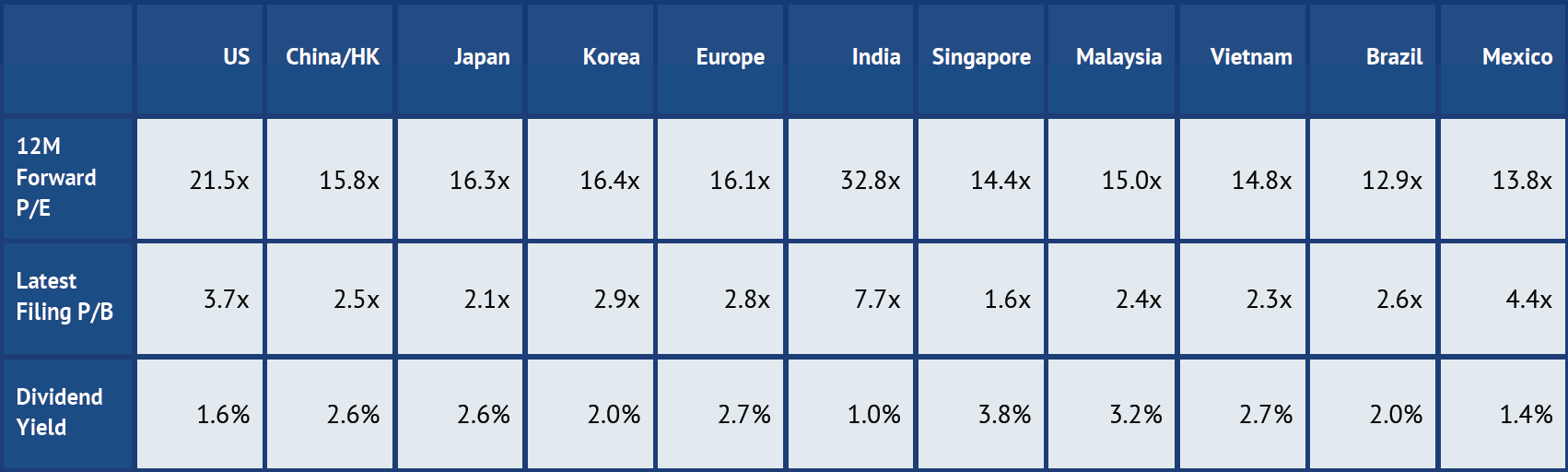

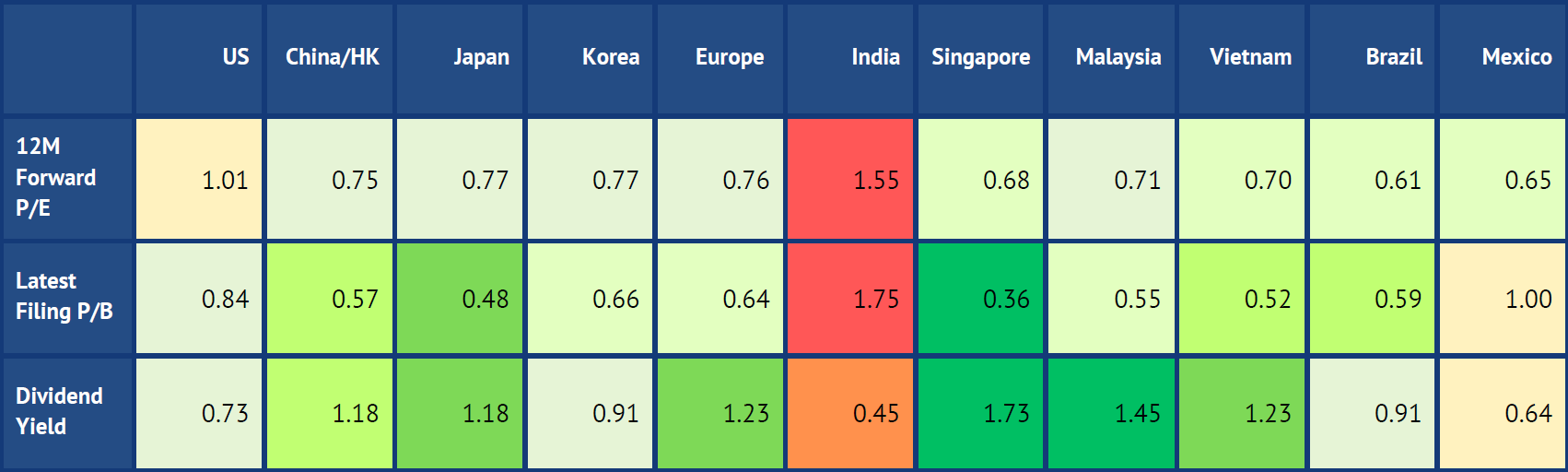

Valuations Snapshot

Current valuations

Relative to 10-year historical

Relative to Global Equities

Source: Bloomberg

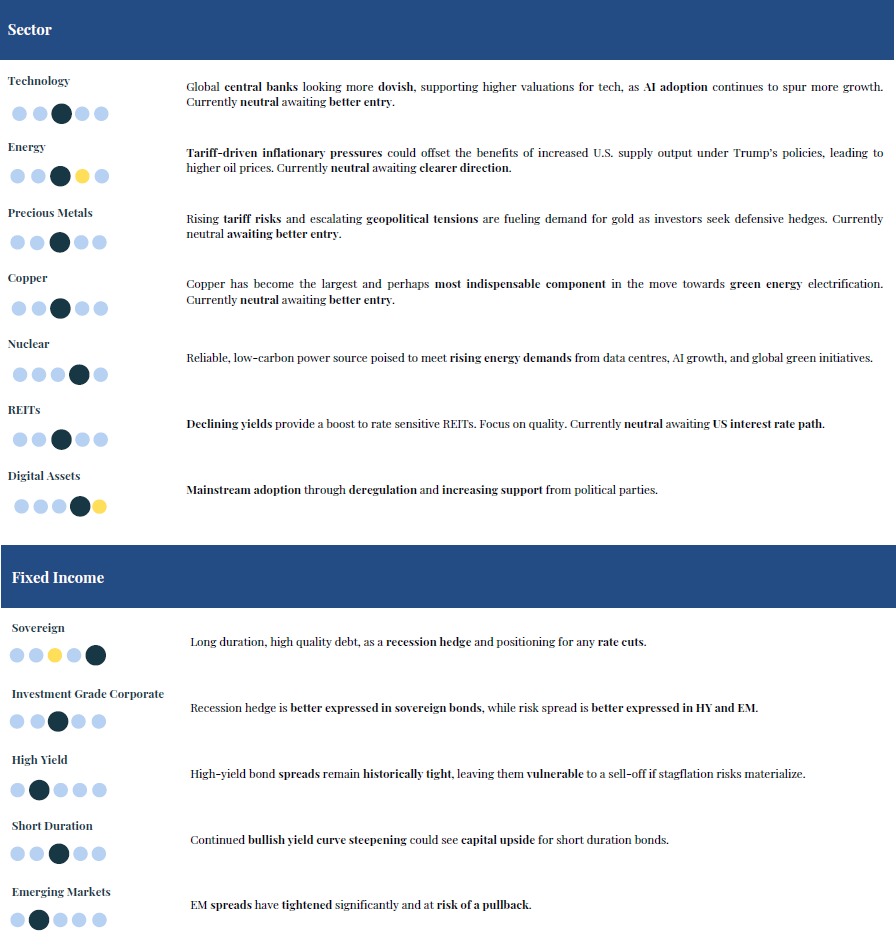

Tactical Views

Disclaimer

This publication is for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or risk tolerances of any of the recipients. The information or opinions provided are personal views and do not constitute investment advice, a recommendation, an offer, or solicitation to subscribe for, purchase, or sell the investment product(s) mentioned herein.