Monthly Investment Insights - Apr 2025

The Empire Strikes Back

Source: Bloomberg

Market Review

March proved to be a dismal month for financial markets, bringing the S&P 500 to its worst first quarter since 2022 with a decline of 4.6%. This significant downturn was primarily driven by mounting uncertainty surrounding President Trump's economic agenda, particularly his escalating tariff threats and the looming April 2 trade deadline. These developments have sparked serious stagflation fears across markets. The chart above shows the Atlanta Fed's Q1 GDP estimate a concerning 2.8% contraction, while inflation expectations remain elevated, with tariffs being identified as a major contributing factor.

In China, markets experienced a notable retracement after weeks of upward momentum. This pullback was attributed to profit-taking, a lack of positive catalysts, and defensive positioning ahead of the April 2 US trade deadline. Additionally, share placements by major companies like BYD, Xiaomi and Nio further dampened sentiment.

Performance

My March exposure was negatively affected across all asset classes, with US equities declining 4.6% amid escalating tariff threats and stagflation fears. The nuclear sector suffered an even steeper decline of 7.6% on demand fears, while US treasuries retreated 1.2% as yields climbed higher in response to stubborn inflation. Digital assets were particularly volatile, with Ethereum plummeting 17.7% and Bitcoin showing relative resilience with a more modest decline of 2.3%, highlighting the risk-off sentiment.

Outlook

April is poised to be a historically significant month, with April 2 being coined "Liberation Day" by Trump. On this date, the Trump administration is expected to announce a raft of new tariffs, potentially escalating growing trade tensions with some of America's closest allies. The scope and severity of these measures—whether selectively targeted with leniency or aggressively broad-based—will likely determine the trajectory of financial markets for months to come. Market participants are particularly concerned about potential retaliatory measures from the EU, Canada and China, who have already signalled readiness to respond in kind to any punitive actions.

With stagflation concerns mounting and the "Trump put" seeming increasingly unlikely, markets appear to be pivoting their attention back to the "Fed put," with interest rate futures now suggesting three rate cuts this year to counteract deteriorating economic conditions. In my opinion, Trump's uncompromising approach thus far suggests a calculated strategy to force Powell's hand in cutting interest rates, thereby achieving his economic trifecta: protective tariffs, accommodative monetary policy, and a strategically weakened USD. This combination, in Trump's view, would address persistent US trade imbalances, reinvigorate domestic manufacturing, substantially reduce government interest expenses, all while supporting a robust stock market.

Allocation

For April, I maintain a positive outlook on U.S. equities and long-term Treasuries, and added mortgage backed securities, anticipating that stimulus measures will help alleviate stagflation fears. I view the nuclear energy sector's recent pullback as overdone, with structural demand remaining intact. Digital assets stand to benefit from deregulation tailwinds and increasing allocation from institutional investors, listed companies, and sovereign reserves.

Overweight Picks & Performance

*Edited 2 Apr 2025

*Since 2 Jan 2025

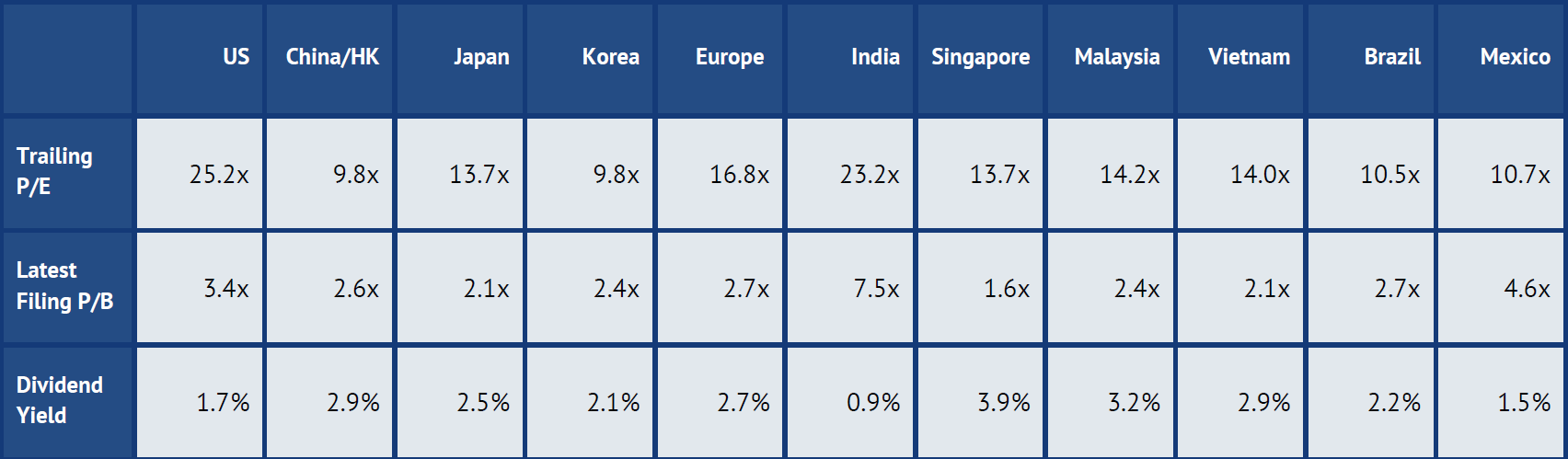

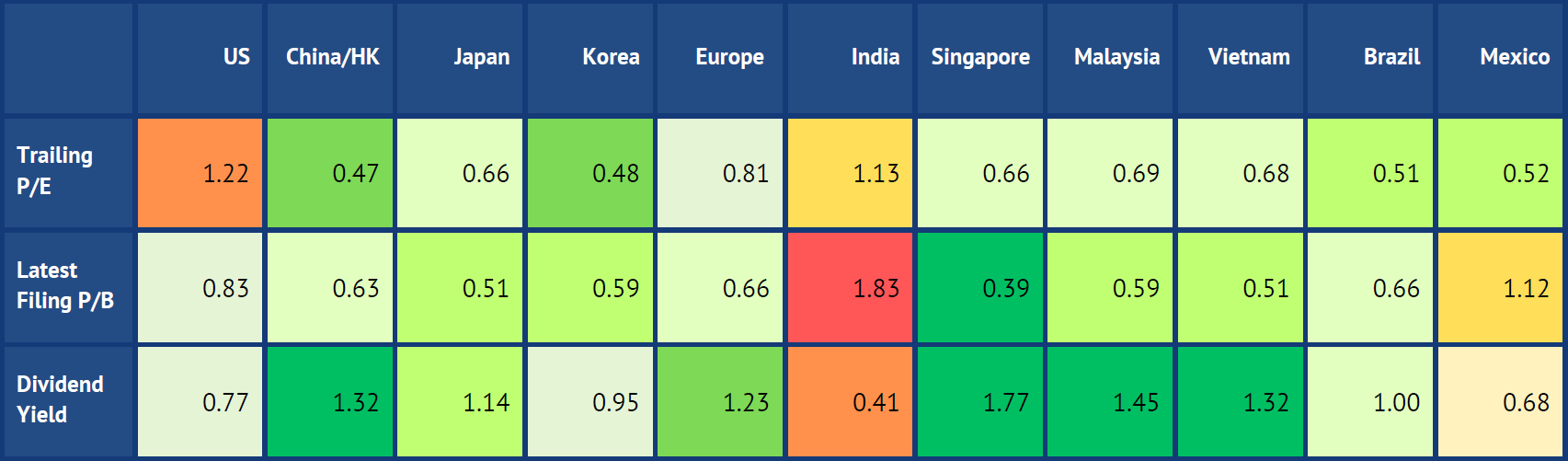

Valuations Snapshot

Current valuations

Relative to 10-year historical

Relative to Global Equities

Sources: Bloomberg, WorldPERatio

Tactical Views

Disclaimer

This publication is for informational and educational purposes only. There is no consideration given to the specific investment needs, objectives, or risk tolerances of any of the recipients. The information or opinions provided are personal views and do not constitute investment advice, a recommendation, an offer, or solicitation to subscribe for, purchase, or sell the investment product(s) mentioned herein.